Forecasting the Unemployment Rate in Malaysia using ARIMA Models

Keywords:

Unemployment rate, ARIMA, time series analysis, structural breaksAbstract

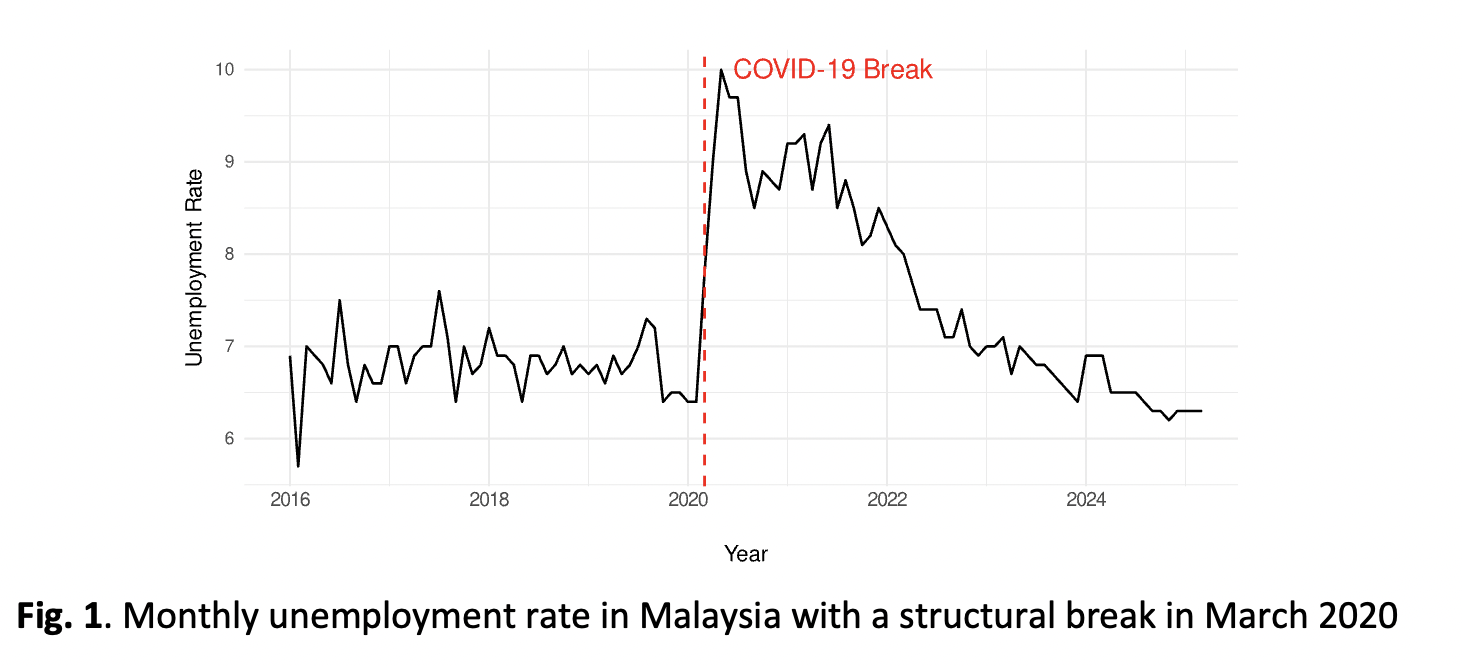

Considerable fluctuations in Malaysia’s labour market have been driven by both global economic uncertainties and domestic transformations. Events such as the COVID-19 pandemic exposed the labour markets to certain vulnerabilities. Gaps remain in the literature regarding the continuous validation of forecasting models of the unemployment trend in the presence of extreme events such as COVID-19, particularly over extended and post-pandemic periods. It is essential to develop an

accurate forecast for unemployment trends to inform effective labour market policies and economic planning. This study analyses the monthly unemployment rate in Malaysia from January 2016 to March 2025 with the aim of modeling and forecasting Malaysia’s monthly unemployment rate using a time series approach. A structural break analysis, assuming one break, identified a significant change in trend occurring in February 2020, which aligns with the onset of the COVID-19 pandemic. This suggests that the pandemic had a notable impact on the labour market. The identified break point is then used as a basis for modeling the data using ARIMA, considering the change in trend to improve forecasting accuracy. Two distinct forecasting models are developed: one assumes no pandemic, using data before February 2020, and the other reflects the post-pandemic period. The forecasts for both periods highlight how the pandemic altered the unemployment trend and model structures. These findings underscore the importance of accounting for structural breaks in time series modelling to improve forecasting accuracy and provide critical evidence for labour market policy and planning in line with the United Nations Sustainable Goal (SDG) 8.