Management Accounting Practices for Decision-Making of the Listed Manufacturing Organizations in Bangladesh

DOI:

https://doi.org/10.37934/arbms.39.1.118Keywords:

Management accounting practices, manufacturing, decision-making, BangladeshAbstract

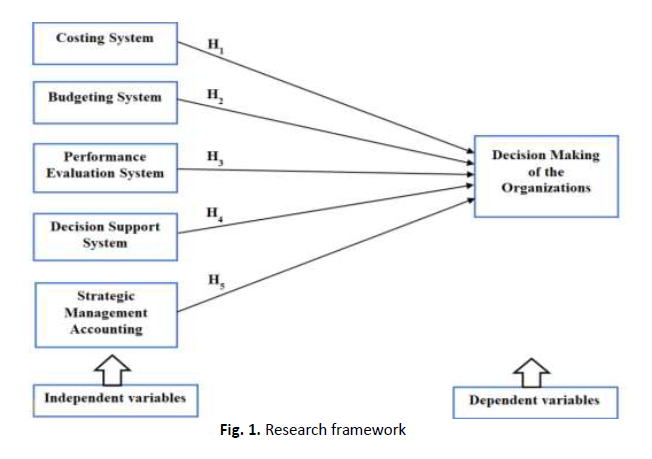

This paper investigates the relationship between management accounting practices (MAPs) and decision-making processes (DMPs) within manufacturing organisations in Bangladesh and examines the extent of use of various MAPs, including costing systems, budgeting systems, performance evaluation systems, decision support systems, and strategic management accounting analyses for decision-making (DM). By utilising descriptive statistics, multiple regression, and Pearson correlation tests, the study examines the relationship between these practices and decision-making. This is achieved through the administration of a structured questionnaire to 70 respondents representing 35 DSE-listed manufacturing enterprises in Bangladesh. SPSS version 25 is used to test these results. The findings reveal significant positive relationships, indicating that specific MAPs significantly influence DMPs. Notably, process costing, budgeting for planning and controlling costs, a variety of financial performance evaluation systems, cost volume profit analysis, and shareholder value analysis. This study provides empirical evidence that highlights the information generated by various types of MAPs that are important for decision-making in manufacturing organizations in Bangladesh. The study suggests implications for practice, highlighting the importance for manufacturing organisations to carefully consider their use of MAPs to enhance decision-making effectiveness. The study's limitation lies in its exclusive focus on the MAPs of manufacturing companies in Bangladesh, underscoring the need for further research that encompasses both the manufacturing and service sectors.