Performance Analysis of Conventional and Islamic of Real Estate Investment Trust (REITs) in Malaysia

Keywords:

Malaysian REITs; Sharpe Ratio; Jensen Ratio; Treynor Ratio; Conventional REITs; Islamic REITsAbstract

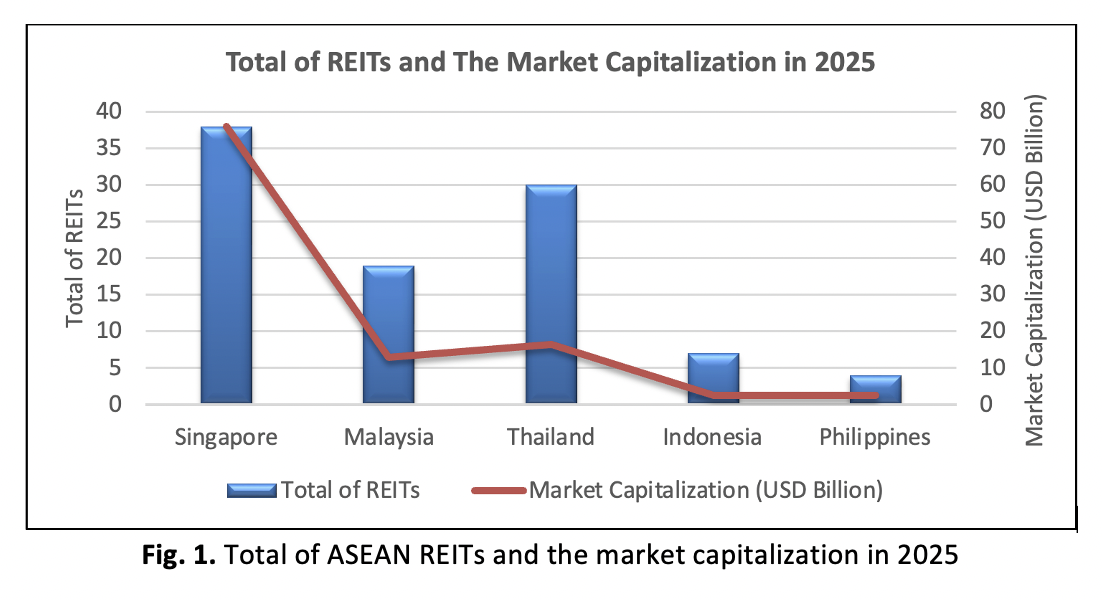

This study investigates the risk-adjusted performance of Malaysian Real Estate Investment Trusts (M-REITs) by comparing Conventional REITs (C-REITs) and Islamic REITs (I-REITs) over the period from January 2018 to January 2026. Grounded in Modern Portfolio Theory, the research evaluates how effectively these investment vehicles generate returns relative to the level of risk undertaken, while also examining their resilience under varying economic conditions, including the COVID-19 pandemic and post-pandemic recovery phase. A quantitative research design is employed using daily secondary data sourced from Bursa Malaysia, with the FBMKLCI and EMAS Shariah Index serving as market benchmarks. The Sharpe Ratio is utilized as the primary measure of risk-adjusted performance, supported by the Treynor Ratio and Jensen’s Alpha as robustness checks. The findings indicate that both Conventional and Islamic REITs generally exhibit weak risk-adjusted performance, as reflected by predominantly negative values across all performance measures. However, Islamic REITs demonstrate relatively better performance compared to their conventional counterparts, suggesting greater efficiency in managing risk due to their Shariah-compliant structure and conservative financial practices. Furthermore, both categories of REITs show resilience by outperforming their respective benchmark indices during certain periods, highlighting their role as defensive assets within diversified portfolios. Overall, the study contributes to the existing literature by providing a comprehensive and comparative evaluation of Malaysian REIT performance using multiple risk-adjusted measures, offering insights for investors, policymakers, and financial institutions regarding the effectiveness and stability of REITs in Malaysia’s capital market.